Market Watch Diary: Wild Cards at Play

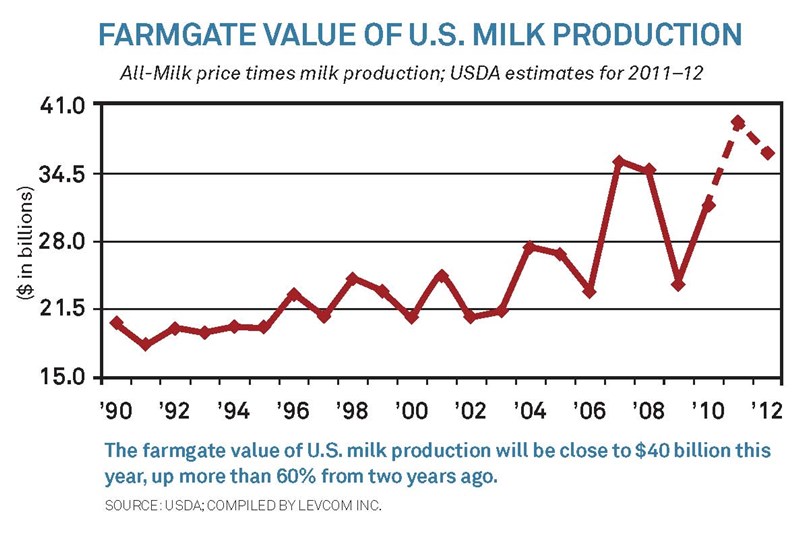

These are heady times in the dairy business, with $20-plus per cwt. checks showing up in your mailbox alongside your issue of Dairy Today. Even with feed and other costs at all-time highs, profitability has generally returned to pre-crash levels. The farmgate value of U.S. milk production will be close to $40 billion this year, up more than 60% from two years ago.

These are heady times in the dairy business, with $20-plus per cwt. checks showing up in your mailbox alongside your issue of Dairy Today. Even with feed and other costs at all-time highs, profitability has generally returned to pre-crash levels. The farmgate value of U.S. milk production will be close to $40 billion this year, up more than 60% from two years ago.

But we’ve learned we shouldn’t get too drunk on rarified air. With global stocks at all-time lows, the markets are particularly susceptible to shocks of any kind. Virtually any wild card could alter the global situation. Three big factors to keep an eye on:

China and Russia. Since 2007, these two countries have accounted for nearly three-quarters of the global increase in dairy trade, according to numbers from the Food and Agricultural Policy Research Institute (FAPRI).

Russia, which was forced into the world market heavily last year to offset drought-related domestic shortfalls, curtailed imports in the second quarter, causing a bit of a backup. China’s purchases have continued, but some of that was inventory building. Buyers are taking the summer off to see how New Zealand’s new season develops before overcommitting for the fall and winter.

Bonus Content |

| FAPRI 2011 World Agricultural Outlook USDA's Dairy Market News biweekly prices and yearly summaries |

Price resistance. Global dairy commodity prices have been trading in a higher band for 12 to 18 months. So far, buyers and consumers have been willing to absorb the increases. The biggest difference between the 2007 runup and now: Then, prices doubled in a matter of months; this time around, the gains have been more measured.

Still, commodity trade is guided by a herd mentality. If there’s even a hint of demand resistance and the market starts to turn, sellers will price more aggressively to keep inventories from building.

Weather. More than ever, we have to expect the unexpected from the skies, oceans and earth. Climate change makes weather disruption a regular occurrence. As of this writing, milk production conditions are favorable in the Southern Hemisphere and OK in the Northern Hemisphere. But that could easily change with the next drought, earthquake, flood or blizzard.

The "what-ifs." No doubt there are other wild cards in the deck. Maybe high milk prices will spark greater than expected dairy expansion here and abroad. Maybe a change to domestic dairy or food policy will tweak the way we do business. Maybe shifts in the costs of inputs or energy will upset existing production models.

Some political or military crisis might alter trade flows. Perhaps another global financial crisis is looming around the corner.

In the meantime, enjoy your record-high milk check. Things look good now, but dairy has proven to be a very unpredictable business.

ALAN LEVITT is president of Levcom Inc. in Crystal Lake, Ill. You can contact him at (815) 459-1742 or alevitt@levcom.com.