Market Watch Diary: Weaker Markets Forecast

Forecasting the dairy markets has almost become a fool’s errand, because of the frequency with which "black swan events" turn our outlooks upside down.

Forecasting the dairy markets has almost become a fool’s errand, because of the frequency with which "black swan events" turn our outlooks upside down.

There is no "normal" anymore. Something unpredictable is lurking out there—a climate event, an economic incident or maybe a political episode.

That said, the rump end of the year is the time for outlooks, so here’s what my crystal ball says for 2012:

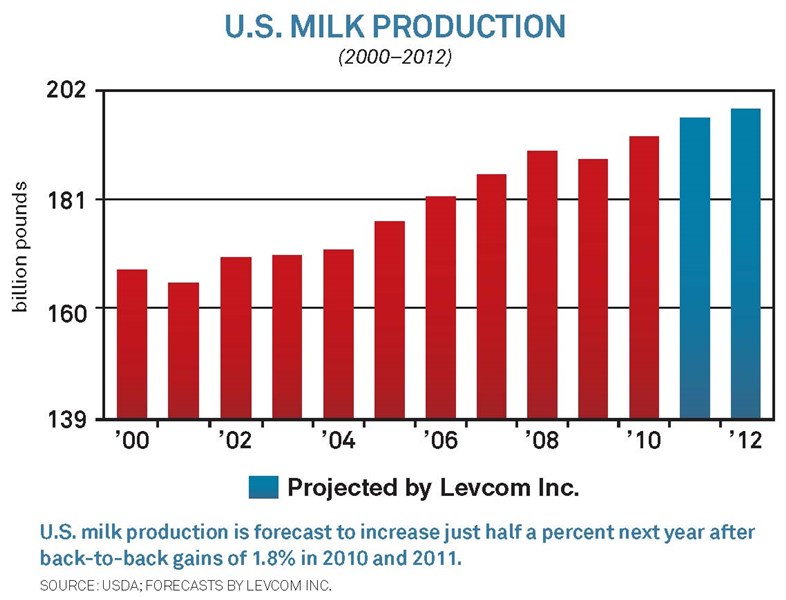

Continued growth in U.S. milk production through the first half of 2012. With the lags in the system, producers should still get $20 milk checks in November and December, forestalling culling. I’m forecasting milk production growth of about one-half percent overall next year, with first-half gains mostly offset by second-half contraction.

Weaker world market conditions will put downward pressure on the U.S. market. In the first three quarters of this year, milk production from the five major export suppliers was up nearly 3% from the prior year, and the brakes haven’t been applied yet. Demand has proven to be resilient, but at this point it can’t keep up with the rate of expansion.

Bonus Content |

| Growing U.S. milk production |

Steady domestic consumption, but slower export sales. When world dairy market conditions soften, the U.S. has historically lost export market share. I think we’ll do better than we have in the past, but we’ll still see a sales decline.

A $17.00 to $18.50 per cwt. average All-Milk price. This may be good by historical standards, but in today’s world it will create margin pressure, particularly in the first half of the year. I don’t expect margins to get as bad as 2009, but look for something similar to 2006.

Which brings us back to the "black swan." By definition, this will be something unforeseeable, but if I had to lay odds, I’d say there’s a greater chance the next curveball is going to have a bullish, rather than bearish, effect. We almost have to expect one or more bizarre weather phenomena every few months, which generally serves to tighten the market.

Feed costs have become particularly susceptible to shocks, which will play a big role in dairy farm profitability. Meanwhile, global dairy suppliers don’t carry the level of buffer stocks they did in the past. Production is heavy now, but any disruption in the supply chain could change the outlook in a hurry.

ALAN LEVITT is president of Levcom Inc. in Crystal Lake, Ill. You can contact him at (815) 459-1742 or alevitt@levcom.com.